This is the Part 2 of the article about UITF, Mutual Fund, and VULs, the so-called “pooled funds“. Here is the first article in case you have not yet read about it:

This is the Part 2 of the article about UITF, Mutual Fund, and VULs, the so-called “pooled funds“. Here is the first article in case you have not yet read about it:

Difference between UITF, Mutual Fund, and VUL

Now, we are going to discuss where these funds invest your money. As I mentioned before, they invest in securities of different classes. Let us expound on each one of these classes.

What are the securities where these funds are being invested?

We call them, Asset Classes, which are a group of individual securities or investments that have a common financial form like common stocks, bonds, real estate and others.

They usually perform in a similar fashion distinct from other asset classes.

These are the major asset classes:

- Cash and Money Market Instruments

- Fixed Income (Corporate/Government Securities)

- Stocks/Equity

- Real Estate

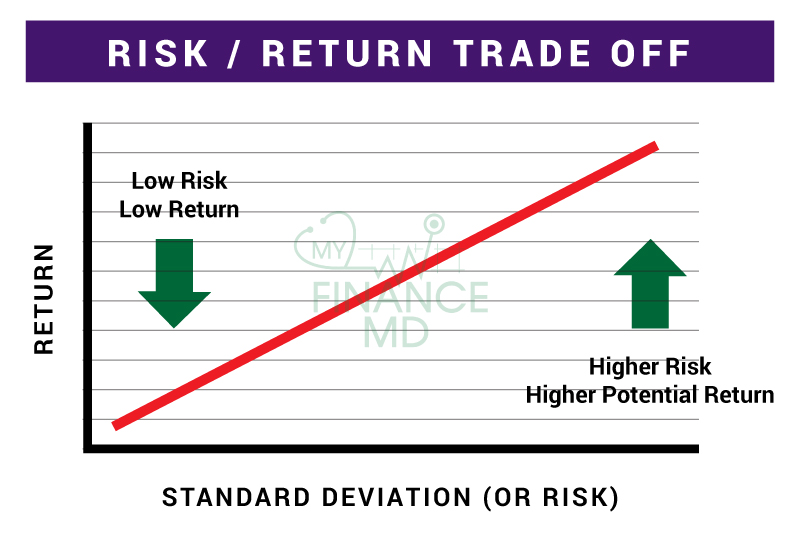

Before we discuss each of them, let me show you the basic concept where these funds operate.

They operate in this concept. The higher the return on investment (ROI) you would like to have the higher the intrinsic risk the investment has. Higher risk means higher chances that your money will fluctuate, go up or down. The safer you want your money, the lower return you will get from it.

Let’s proceed from discussing each one of them.

1. Cash and Money Instruments

These are instruments that are low risk, low yield.

Examples of these are:

- Money in Bank

- Bank Certificates or Time Deposits

- Treasury Bills

- Short term loans by the Philippine Government issued by the Bureau of Treasury. Example: 91 days, 182 days, 364 days T-Bills.

- Commercial papers

- Short Term loans by corporations – these are loans the money earns thru interest rates.

2. Fixed Income (Corporate/Government Securities)

These are instruments that are low risk, low yield.

- Corporate Bonds – these are debt instruments issued by the corporations (borrowers) to bondholders (the lenders). Bonds earned by the interest which pay out a fixed rate for a specified period of time and the return of the principal at the maturity date.

- Government Securities – debt instruments issued by the Government (the borrower) to bondholders (the lenders). Interest payments and repayment of principal is guaranteed by the government.

- Treasury Bill

- Treasury Bond (Retail Treasury Bonds, Fixed Rate Treasury notes, ROP Bonds)

How does it work?

When we say bonds, it means “utang” in Filipino. For example, if you loan in a bank, the bank will earn from you by letting you pay interests, right? That’s the same with bonds. If you invest in “bonds” it means that the government or the corporation has a loan from you. You will earn from them when they pay “interest for you’.

The above figure is an example of how a government security like a Treasury Bond works. As you can see, the lender earns 4% every year and at the end of the term will get back her principal.

3. Stocks/Equity

Stocks are also called Equities which represent an ownership stake in a corporation. Stockholders are part owner of the company.

When investing in stocks, you must consider:

- It is a high risk, high return investment instrument.

- These are the stocks listed in the stock market. In the Philippines, it’s the PSE or Philippines Stock Exchange.

- The value of share fluctuates according to the market’s view of the worth of the company.

- Prices may increase or decline significantly.

- The investor earns when he buys stocks at a lower price then sells his stocks at a higher price.

4. Real Estate

This is another class where your pooled funds may invest your money into.

These are land plus anything permanently fixed to it, including building, sheds and other items attached to the structure.

The investor earns when the value of real estate appreciates over time. The value of real estate is primarily affected by local factors.

A Sample of Appreciation of Land:

A piece of land in Cavite is priced at 7,500/square meter last 2003, after some developments seen in the area like a building of malls, highways, and condominiums, the value of the land appreciates. When these lands are now sold, they are priced at 30,000 – 50,000/square meter.

A Sample of Depreciation of Land:

Before 2009, a posh subdivision in Marikina, Provident Village sells at a very high price and everyone wants to buy, but when Typhoon Ondoy (2009) came and the subdivision became one of the hardest hit, they realized that the location is a catch basin of Pasig River. The people who bought begun selling and the price go down as no one wants to buy. A property sold 5 Million before 2009, now, is being sold at 1 Million, and still no one wants to buy.

Although depreciation of a real estate is possible, a real estate broker friend told me it is just one in a hundred. Real estates are still good investment especially if the investor carefully studies the location and different risks the land may encounter.

Technically those are the different securities where your “pooled funds” invest into. The main advantage of pooled funds (UITF, MF, and VUL) is the “pooling of funds” where your money is part of a bigger pool of investment. You have the advantage of investing in all asset classes whereas if you are just an individual investor (those investing on their own) and only have 5,000 pesos investment or a limited budget, some asset classes requires a minimum investment, so those with limited funds cannot invest in those asset classes that have a minimum required investment.

Pooled funds allow diversification of your investment even with just a very minimal investment. Since they pool your money along with a big pool of money of other investors, the investment power of your money is increased.

Wait for more, in the Part 3 of this series, I will be discussing about:

The Different RISKS of your investments.

Don’t forget to like MYFINANCEMD FB page to be updated with this series.

Contact me here if you have any questions or if you want to get a personalized financial health check-up!

By the way, I am licensed in providing: UITF, Mutual Funds and VUL products. Contact me here if you want to start now.

For your Financial Health,

Read more:

- Difference between UITF, Mutual Fund, and VUL

- Single Pay Investment with Life Insurance (A Super Product for Lazy Investor)

- The BEST INVESTMENT Vehicle for Your Child’s Education

- Investment Scams: How Not to be a Victim?

Sources: UITF, Mutual Fund Handbooks, My Real Estate Friend

Latest posts by Pinky De Leon-Intal, MD, RFC (see all)

- Say Goodbye to Chronic Lifestyle Diseases (Hypertension, Diabetes, Cancer, Gout, etc.) with Right Food and Right Water - 23 May, 2023

- Embracing Superpowers: A Mom’s Journey as a Doctor, Professor, and Financial Consultant - 19 May, 2023

- Celebrating the Power of Women: Honored by Philippine Daily Inquirer - 17 May, 2023