Credit cards are just small plastics cards. They may seem small and harmless in your wallet but they are one of the most powerful inanimate objects I know that can give people sleepless nights and untreatable headaches. The purpose of this post is educating the first time credit card users but it can also educate some old users that are trapped in the power of this small plastic card.

Credit cards are just small plastics cards. They may seem small and harmless in your wallet but they are one of the most powerful inanimate objects I know that can give people sleepless nights and untreatable headaches. The purpose of this post is educating the first time credit card users but it can also educate some old users that are trapped in the power of this small plastic card.

This small plastic card holds great power. Power to win and lose. Such power requires great responsibility, here are the things you need to know:

1. Know your credit limit

The most important thing to check first if you are a first time credit card user is your credit limit. This ranges from a few thousands to 100,000 or more, depending upon your approved limit. This will be dependent upon how the bank evaluates your income, your work stability and your ability to pay. This is the limit of the spending power of your credit card. You can only spend up to this limit.

2. Treat your Credit Card as Cash

Once you know your credit limit, don’t fall into many first time credit card user’s mistake to treat it as an “extra money“. Rather, you should treat it as just an alternative to “Cash“; cash that you already have now but don’t want to carry around.

3. Don’t be misled by “Minimum Payment”

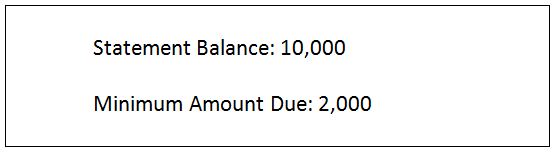

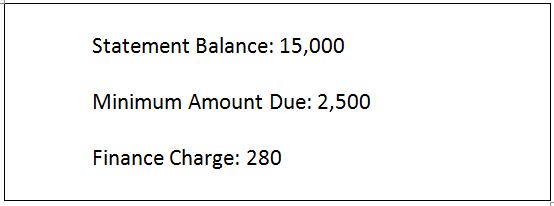

When I was a first time credit card user, I didn’t know this. When I got my first bill, it looks like this:

When I saw the bill, I said to myself: “Wow, it means I can only pay 2,000?” And that was what I did, until the reality hits me when the next bill arrives.

So, that’s what happens when I just pay the minimum amount due. Another type of charge appears; the finance charge.

4. Know the interest rates in case you can’t pay on time and in full

Credit card charges are the highest interest in the loan industry. They range from 3% – 3.5%, depending on the bank.

If you think, it’s just 3%, how did it become the highest?

To answer that question: Well, you have to know that it is PER MONTH, and not PER ANNUM. Let us compare it from other types of loans, per annum:

Housing loan: 5 – 10%/year (depending on number of years of loan) see housing loan rates here

Car loans: 7 – 12 %/year (depending on number of years of loan)

Personal loans: 15 – 22%/year (depending on amount of loan and number of years of repayment)

Credit Cards: 36 – 42%/year (amount not paid in full and on time)

5. Know your “cut-off-date” and “due date” if you are using your credit card to buy you some TIME

Well, one good thing good you can get from a “credit card” is that it can buy you some time. For example, you need to buy something now but you still don’t have the cash, knowing your salary is just 5 days away, then you can use your credit card to buy you some TIME.

But as I said, if you don’t want to fall into a credit card trap, go back to rule #2, treat it as cash. Once you receive your salary, pay it off ASAP.

If you want to buy some time, at least you should know your “cut-off-date”, it is a day in a month where your bills are generated and your “due date,” the day you need to pay up without generating interest. For example, my “cut-off-date is every 1st of the month and my due date is every 15th. That means:

The bill’s due date will appear on the actual billing statement. June 2nd to July 1st is called the “billing period”. July 1st would be called the “cut–off date“, the “closing date“, or sometimes the “billing period end date”. July 15th is most commonly called the “due date“ or “payment date”.

6. The Dangers of “Zero % Interest”

One of the most attractive features of a credit card is the “Zero % Interest Promos”. With this, you can buy “big ticket items” for installment for few months, or even years, without generating interest. This makes your small plastic card even more powerful.

Suddenly, you can now buy the best gadget, the Mac Book you’ve been dreaming of, the Smart LED TV you so wanted a few years ago.

From my actual experience: Few years back when our house is new and needed many appliances, I just use the card and swipe “12 months zero interest”. It was a happy and exciting feeling when you can get what you need and want and pay for it later. But after sometime, I am not happy and excited anymore, it’s actually draining. It’s like a never ending load you carry on your shoulder, and for how many months? 12 months or even 24 months? Oh, the feeling sucks! Believe me.

Note: If you are going to use this feature –

All I can say is, you have to know the dangers. I have been attracted and trapped in this “Zero % interests” few years back, it was “difficult” and I don’t want to go back there again. But I am not totally dismissing the fact, that I may do it again, but now, if I really need to go back there again, I made a rule for myself, “one-at-a-time” and “as quickly as I can”.

When I really need to buy something, what I do now is to save for it for months before buying. I still use my credit card, yes, because I don’t like bringing big cash in my wallet, and of course I want to get my credit card points. When I already have the cash, that’s the time I buy.

I so love this part:

Cashier: “Installment for 6 months ma’am?”

I answer: “No, charge it as straight!” (meaning, charge the whole thing not installment)

I can feel the cashier’s secret admiration, or so I think. Then, I feel good. Not that I am being “mayabang” but I feel proud that I have instilled the discipline to myself of planning and saving up first before buying.

7. The “Credit Card Rewards and Rebate System”

A mentor once told me a story about his conversations with a credit card company owner. Let me tell you the story:

Mentor: “Who is your best client? Is your best client the Platinum Card holders?”

Credit Card Company Owner: “Heck no, actually they are our WORST clients. Yes, they have an unlimited credit limit, they do have big purchases, and they even purchase everything using our credit card. But the problem is, they pay ON TIME and IN FULL. We can’t get anything from them, yet, they reap all the REWARDS. Free trip abroad, free hotel stays, free spa, free food and free gifts.”

Mentor: If you are not earning anything from them, who pays for their Rewards?

Credit Card Company Owner: “Ah, well that is paid for by our BEST clients.

Mentor: Who are they?

Credit Card Company Owner: The best clients that we have are the CLASSIC OR REGULAR card holders, the one that have a smaller credit limit. The one that makes their purchase but DOES NOT pay on time and in full. That’s where we gain more because of the charges. They are also the ones that pay for the rewards of our worst clients, the trip abroad, the hotel accommodation, the free gifts and free foods.

That conversation says it all; there goes the lesson on rewards.

When choosing a credit card, choose the best reward system that can give you more edge depending on your lifestyle.

If you are a frequent flyer, you may opt to choose a card with “Premier Miles” the one that gives you “free trips” on your trips.

If you love cars and driving, you may opt to choose a card that gives you 1-3% rebates whenever you gas your car.

If you love shopping, get a card that gives you higher rebates when shopping.

There are a lot more, do some research and find the best card that you can get that will suit your lifestyle and your needs.

After learning all these 7 golden lessons I am giving you today, I am happy to tell you that, now:

- I treat my credit card as cash now.

- I don’t use it if I don’t have cash to pay for it that very same day of using it.

- I am gathering up my rewards points, and planning to use it to buy me a free ticket to a trip to maybe U.S. or Canada.

- I have been having free food, free watch and even free spa with my credit card rewards.

As, the saying goes:

The more you know, the less you pay!

For your financial health,

PS: Another advance warning: Some people may ask you: “Pa-swipe naman sa card mo” Usually they want the installment feature when they want to buy something they can’t pay cash. Then it’s your call if you want to be their superhero, but if you are to ask me, the answer is a “no-no”.

Do you want me to be your personal Financial Doctor and Your Wealth Planner? Contact me here!

Don’t forge to like me on Facebook!

Read more:

- Credit Cards: The Bad, the Ugly and the Good

- How to Win the War? You Vs Your Debt

- Top 14 Illnesses of a Financially Sick Filipino

- Code Blue: Resuscitate Your Finances using CPR

Latest posts by Pinky De Leon-Intal, MD, RFC (see all)

- Say Goodbye to Chronic Lifestyle Diseases (Hypertension, Diabetes, Cancer, Gout, etc.) with Right Food and Right Water - 23 May, 2023

- Embracing Superpowers: A Mom’s Journey as a Doctor, Professor, and Financial Consultant - 19 May, 2023

- Celebrating the Power of Women: Honored by Philippine Daily Inquirer - 17 May, 2023

Very well explain Doc Pinky. I am so glad that I have those ideas before and I have major in accounting leads me to always do the math😊and was able to share the same to my colleagues who had wrong used of cc.

Please allow me to share some things that I experience and do on credit cards

1.Waiver of Annual Membership-usually pemium is waive on the first year but almost all credit cards allow to have it waive once you call them after you received your annual membership bill. On my almost 20 years of using cc I never pay for my annual fees,if they insist,I just tell them I will have it cancelled,fortunately they waive it so I wont cancel my card.

2.Waiver of interest/finance charge -there were times that I forgot paying my bill on time ,last experience was I received immediate due date because I guess its almost 15 days delayed,I just called and requested to waive the finance and penalty charges after paying my account in full,stating my reason that I missed the due date, they are generous enough to waive it if they see that you are valued client.

3.In addition to zero percent, mostly it is not really a zero percent on appliance,gadget etc,because when you ask them how much the cash price or straight payment they will give you discount.It only means that the interest is already incorporates on the said “O%”,so I always go for straight charge if there is discount.

regards and more power!

Thanks for sharing. Others will learn from you too. 🙂