Before we start with the Guide to Creating your Beneficiaries to your life insurance policy, let me familiarize you with some of insurance lingo and terms that we will be using in this post:

Before we start with the Guide to Creating your Beneficiaries to your life insurance policy, let me familiarize you with some of insurance lingo and terms that we will be using in this post:

Policy Owner (or policyholder) – the person who owns an insurance contract (policy)

Life Insured – The person whose life is insured. This could be you, but it doesn’t have to be.

*Most of the time the Policy Owner is also the Life Insured. But not all the time.

*Cases where Policy Owner is not the same as the Life Insured. When you get a plan for your child, a parent will be the Policy Owner and the Life Insured is the child.

Premium – the amount of money you pay to buy insurance. You can pay the premiums monthly, quarterly or annually.

Policy – this is also called the life insurance contract. The legal agreement between you and the insurance company that sets out the terms of the insurance you buy. It includes the application forms you filled and signed, the policy itself, and the terms and conditions.

Death Benefit – also called the proceeds or the assured amount.

Trustee – a trusted legal adult who is designated by the insured to manage and supervise the money (death benefit) for the children’s benefit if the beneficiary is still a minor

Now let’s go to the main topic:

Guide to Creating your Beneficiaries

1. What is a ‘Beneficiary’?

The person who will receive the proceeds or the death benefit payable under your insurance policy.

2. Who can be a beneficiary?

A beneficiary is not just anybody a policy owner wants, there should be an “insurable interest” that exists between the insured and the beneficiary.

What do you mean by “insurable interest?”

Insurable interest exists when an insured person derives a financial or another kind of benefit from the continuous existence of the other.

A person has an insurable interest in the other when the death of the other would cause the person to suffer a financial or another kind of loss.

The Insurance Code – defines “insurable interest” as

Every person has an insurable interest in the life and health:

- of himself, his spouse, and of his children;

- of any person whom he depends wholly or in part for education or support, or in him he has a pecuniary interest;

- of any person under a legal obligation to him for payment of money, or property, of which death or illness might delay or prevent the performance.

Insurable interest exists between the following:

Parents and child (vice versa)

Husbands and wives/ Common law partners

Fiancé and Fiancée

Debtor and Creditor (ang may utang at inutangan)

No insurable interests that exist between the following:

Between Friends

Between Siblings

Between Cousins

If you are making someone your beneficiary with no “obvious” insurable interests with you, you should be ready to defend your relationship with that person so that you can demonstrate “insurable interest’’ between the two of you. Let’s illustrate this in an example:

I have a client who wants to make her aunt her beneficiary. According to the Insurance Code, only the parents to child, not aunt to niece/nephew.

Her defense:

Her aunt took her in when she was still a baby. She gave her a family, support, food, education and made her feel as if she was her own child.

3. A beneficiary could either be: Primary or Contingent

Primary – the person/s who will be the first to receive the proceeds payable under your life insurance coverage when the life insured dies (could be 1 or more persons)

Contingent – the 2nd in line to receive the benefits of a life insurance policy should the primary beneficiary be not present anymore (could be 1 or more persons)

Be careful on deciding if all your beneficiaries will be primary beneficiaries.

I had an experience with this, let me tell you the story. (Based on real story)

Father of 2 died, he only has a 300,000 life insurance policy. He died because of liver cancer. He left her wife a widow, and his 2 grown up sons orphaned, and a big amount of hospital bill, around 300,000.

His primary beneficiaries are the 3, his wife and 2 sons. Being all primary beneficiaries, the 300,000 will be divided into 3. So, they get 100,000 each. The mother, hoping that the 300,000 can pay their hospital bills, came to her agent and asked for help. His sons wouldn’t give her their shares in the policy, leaving the old widow with 200,000 hospital debts and other funeral expenses.

How to avoid this:

Make sure that those people whom you will make primary beneficiaries will take care of your debts and final expenses first before they keep the money for themselves. If you are in doubt, just make 1 primary beneficiary and others as contingent beneficiary.

Contingent beneficiary – will only get the money once the primary beneficiary is no longer around.

4. A beneficiary could either be Revocable or Irrevocable.

Revocable beneficiary – if your beneficiary is revocable, your policy can be changed even without his/her consent. This means you retain all the powers and flexibility in making any changes, withdrawals and even changing the beneficiary without informing the “revocable beneficiary”.

Irrevocable beneficiary – this is the beneficiary where you cannot change anything in your policy without his/her consent. If you choose the Irrevocable beneficiary, every time you change anything from your policy, you need that Irrevocable beneficiary to sign too.

The advantage of Irrevocable beneficiary:

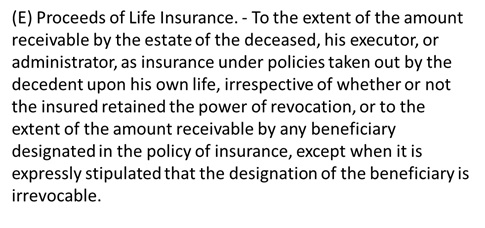

There is such a rule in the TAX CODE:

Meaning: Upon designation of a beneficiary as irrevocable, the life insurance proceeds will not be included any more in the computation of the GROSS ESTATE, thus, protecting the life insured with ESTATE TAXES.

See this post regarding this: What to do to protect and Conserve your wealth?: Part 3 of Estate Planning 101

Important Tip:

Although making a beneficiary IRREVOCABLE has an advantage over Estate Taxes, be careful in naming a minor or child an IRREVOCABLE beneficiary. If you do, you cannot do any changes in your policy until this child/minor would be of legal age capable of making legal signatories.

5. Be careful in making your minor child a BENEFICIARY.

If the designated beneficiary is a minor, the appointed trustee should accomplish the “Claimant’s Statement” or the court approved guardian must submit the following documents:

If the share of the minor does not exceed Php 500,000:

- Duly Notarized Affidavit of Parental Care and Custody. This is to be executed by the mother or the father (whoever is present) if the share of the minor does not exceed Php 500,000.

Or

- Duly Notarized Affidavit of Substitute Parental Care and Custody. This is to be executed by the appointed trustee other than the natural parents if the share of the minor does not exceed Php 500,000.

- Letters of Guardianship shall be required if the minor is orphaned on both parents.

If the share of the minor exceeds Php 500,000:

Besides the needed documents above, here are the additional requirements needed:

- Verified Petition filed in Court

- Decision or Court Order

- Guardianship bond

- Official receipt issued by the Bonding Company

Or, they can have the option to just wait it out until the child turns 18 or of legal age, but, you can just imagine the hassle the people left behind will go through if they want to get the share of the child now.

My suggestion:

- If you trust your partner, make him/her your primary beneficiary.

- Your children could be your contingent beneficiary in order to prevent the hassle of filling court petition which is not very easy just to get the share of the kids.

- Carefully choose the “trustee” for your minor beneficiary, be sure he/she is someone to be trusted.

Generally speaking, making decisions about who your beneficiaries are going to be will be a very important part of your life insurance policy. Make sure you always update itwhen you get married, or get separated or have additional dependents. Also, make sure that the death benefit or the proceeds will be enough to fund for the survival of your dependents. See this post to know if you have enough life insurance: Life Insurance, How much is Enough?

Thinking of making someone who will be your beneficiary is synonymous to thinking of who are the people you love and would love to leave your very last legacy.

For your Financial Health,

Do you want to know you are making the right decisions about your life insurance? Contact me here.

Read more:

- What if I am SICK? Can I still get a Life Insurance Policy?

- 10 Things You Really Should Know About Your Life Insurance Policy You Never Knew

- 5 Insider Tips on Finding the Right Insurance Agent/Financial Advisor For You

- 9 Common Mistakes First-Time Life Insurance Buyers Make and How To Avoid It

Latest posts by Pinky De Leon-Intal, MD, RFC (see all)

- Say Goodbye to Chronic Lifestyle Diseases (Hypertension, Diabetes, Cancer, Gout, etc.) with Right Food and Right Water - 23 May, 2023

- Embracing Superpowers: A Mom’s Journey as a Doctor, Professor, and Financial Consultant - 19 May, 2023

- Celebrating the Power of Women: Honored by Philippine Daily Inquirer - 17 May, 2023

Thanks for this doc.So basically I will practice that as the case permits, it is really a better advice for couples to have their spouse to be a primary irrevocable beneficiary and children as contingent revocable beneficiary and the most trusted relative can be nominated as trustee,right?

Because i used to make the spouse and kids(majority minor) as the primary with equal shares. Thanks doc

Yes, if possible. Of course if spouse is not that trustworthy, it will be a different story. Case to case basis.

Hi Doc,

I would like to ask, does beneficiary’s nationality matter? I mean is it acceptable if a US citizen spouse of an insured Filipina be a beneficiary?

It matters with IRS. They monitor that if US citizens.